Back-to-back! We released our Q1 Bulletin in late March, and while we considered a break, it felt appropriate to release the Q2 Bulletin early. Renewal season is fast approaching, and most of our clients and prospective clients find themselves working through fiscal year start, policy terms, conditions and repricing reset (renew).

July 1 is likely significant for everyone in receipt of this, so let us help you prepare for the insurance impact as much as possible. In our previous "Bulletin," we addressed the challenging market conditions. If you have already renewed your 24-25 terms, you have likely seen or will see substantial increases in rates or retentions, the latter representing the amount of risk your organization assumes before the insurer engages in loss coverage.

At First MainStreet Insurance, we are challenging clients to reimagine how they engage with organizational risk. The insurance market is prompting these conversations. If you are willing to see significant premium increases year over year and don’t have the time or energy to make changes, we support the ‘as is’ renewal approach. But for those who want a different experience, we recommend the use of the acronym “ART” in your risk management conversations. Here’s how:

There are, generally, three ways for you to take on risks that you face organizationally:

- A- Avoid

- Avoiding risk involves changing your operations or business model to prevent a risk altogether. An example of this would be outsourcing work from an internal department and having a third party manage the risk and take on the liability. However, there are likely consequences of this, such as reduced revenue, increased expenses, loss of employees, etc.

- R- Retain / Reduce

- In retaining, and ideally reducing the risk, you acknowledge that you are taking it on and will bear the financial impact of a negative event. You would only want to retain risks that are low in severity, meaning if the event happens it does not have a significant financial impact that would cause you to need to borrow against or liquidate assets. With risks you retain, you want to find risk management practices that reduce both the likelihood and severity of negative events.

- T- Transfer

- Risk Transfer is the area that most think about when considering the insurance industry. By transferring risk, you involve a third party in assuming a portion or all of the liability you have associated with events. One form of transfer is purchasing insurance, where you pay a premium and the insurance company promises to pay for losses you have insured. An example would be paying Insurance Company A $1,500 of annual premium to cover your property damage and bodily injury exposures through a general liability policy with a $1,000,000/occurrence limit. If you are sued and the event is covered under the insuring agreement, Insurance Company A pays up to $1,000,000 for damages, while defending you as it is within the scope of its duty, as a result of you transferring the risk.

I made a challenge to my network on LinkedIn to create a “Risk Register” which required them to think about the risks they take on personally and which of the “ART” forms they used to address those risks. The final call to action was to examine their register and see if we should meet to do this exercise for their overall organization or business. For an overview of the challenge, click here for that LinkedIn post. One benefit is the compilation of my personal list, that could cause me significant financial harm, and how I (attempt) address each.

Because we are known for transferring risks, it begs the question of what we are talking to our clients about in the current insurance market. The reality is insureds are being asked to RETAIN (R) more risk, but how we transfer what we are not forced to retain can still be very strategic. Please understand that not every insurance advisor looks strategically at how to transfer risks. Most are simply looking to renew policies as is. In some cases, that is the best (or only) option.

Our team renews policies depending on the circumstance. However, there is enough change in the market that strategic conversations should be happening on your insurance setup. Even if the recommendation is no changes, you should challenge your advisor to explain why that is the recommendation. There are results to be had, not for every insured, but for the ones with the right risk characteristics, loss history and carrier partners currently engaged.

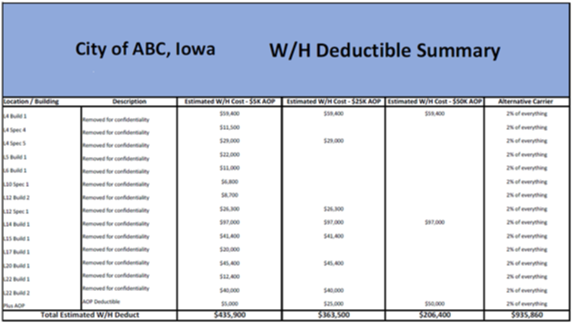

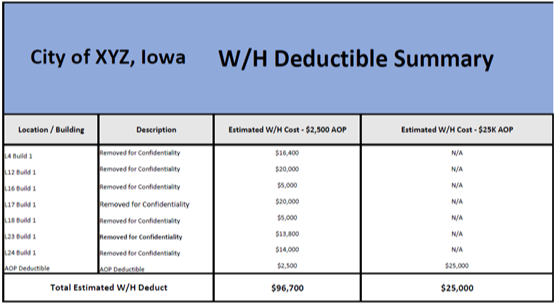

Below are a few of the results we were able to achieve for our Public Entity insureds (names removed for confidentiality) as of April 1, 2024. If any of these looks enticing enough for you to have a conversation about your current Risk Transfer strategy, let’s have a conversation with no obligation to work together for either side of that discussion.